Wide ranging superannuation reforms have now passed through both houses of parliament giving us some much needed certainty around the superannuation landscape. Reforms originally announced in the 2016-17 Federal Budget were further amended in September 2016 and the majority of which will now take effect from 1 July 2017.

There is now a short window of opportunity to both take advantage of current legislation and make preparations for the new more restrictive rules. It is extremely important for SMSF trustees and members to understand the impact of these changes especially in terms of investment strategy, retirement plans and estate planning.

While these reforms will have an impact on most superannuation members you are likely to be significantly affected if:

-

- You are an SMSF trustee

- You plan to make large contributions into super over the next few years

- You plan to increase your super contributions before retiring

- You currently, or plan to, draw a Transition to Retirement Income Stream

- You currently, or plan to, draw a Pension from your superannuation fund

1. Introducing the transfer balance cap

From 1 July 2017, there will be a $1.6 million transfer balance cap on the total amount of accumulated superannuation an individual can transfer into the tax free retirement phase. Subsequent earnings on balances in the retirement phase will not be capped or restricted.

- Savings beyond this can remain in an accumulation account (where earnings are taxed at 15 per cent) or outside the superannuation system.

- Transitional arrangements will apply. People who have already retired with balances below $1.7 million on 30 June 2017 will have 6 months from 1 July 2017 to bring their retirement phase balances under $1.6 million. However, if your balance is over $1.7 million, you may be hit with penalties from 1 July 2017.

- The transfer balance cap will be indexed and will grow in line with CPI, meaning the cap will be around $1.7 million in 2020–21.

| Note |

– The $1.6m cap is per member of the fund, not per fund. Individuals who have multiple superannuation funds will need to carefully consider the total balance of all funds.

– Your overall super balance can be more than $1.6m but only $1.6m can be in a tax-free pension.

– Accurate valuations are critical so that you know where you stand going forward.

– Keeping the excess balance in super, albeit in accumulation phase, may still be worthwhile because of the low 15% tax rate on earnings.

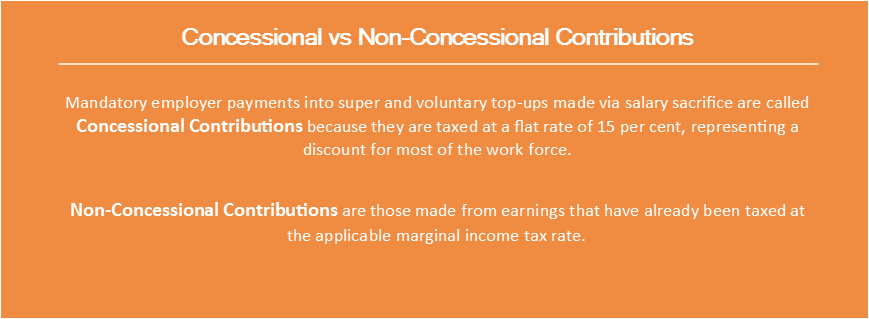

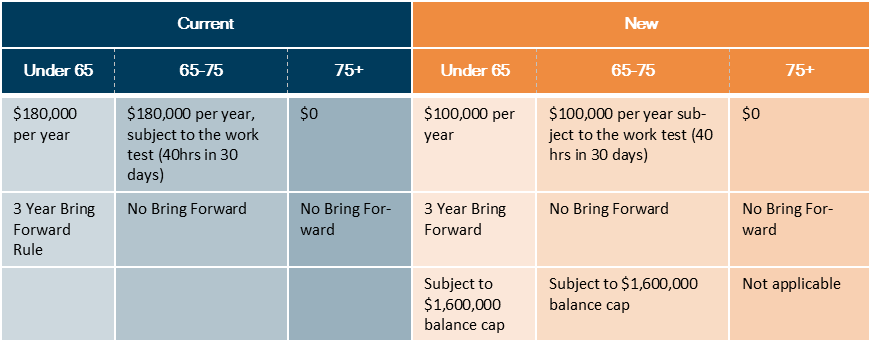

2. Non-concessional contributions cap reduced

From 1 July 2017, the Government will lower the annual non–concessional contributions cap to $100,000 and will introduce a new constraint that individuals with a balance of $1.6 million or more will no longer be eligible to make non–concessional contributions. As is currently the case, individuals under age 65 will be eligible to bring forward up to 3 years of non–concessional contributions.

- The new annual cap with the eligibility threshold replaces the existing $180,000 per year cap.

- The annual cap will linked to the indexation of the concessional contributions caps. The $1.6 million eligibility threshold will be indexed as per the transfer balance cap.

| Note |

– The $1.6 million threshold will be based on an individual’s balance as at 30 June the previous year.

– As is currently the case, individuals aged between 65 and 74 will be eligible to make annual non-concessional contributions of $100,000 if they meet the work test (working more than 40 hours within a 30 day period each income year) but are not able to access the bring forward contributions.

– The 2016/17 financial year will be your last opportunity to utilise the $180,000 cap before it reduces

3. Concessional contributions cap reduced

The threshold at which high income earners pay additional contributions tax (Division 293) will be lowered from $300,000 to $250,000.

In addition, the annual concessional contributions cap has been reduced to $25,000 for all individuals, regardless of age (currently the cap is $30,000 for those aged under 49 at the end of the previous financial year and $35,000 otherwise). This comes into effect from 1 July 2017.

If you contribute over this amount, you will have to pay extra tax.

From 1 July 2018 onwards you can also ‘carry over’ unused portions of your cap for up to five years, as long as you have less than $500,000 in super. For example, if you use $10,000 of your $25,000 cap in the 2018/19 financial year, you would have $15,000 left over to carry over into the 2019/20 financial year.

| Note |

If you are looking to maximise your contributions to super, 2016/17 is your last opportunity to contribute up to the larger cap limits of $30,000 and $35,000 (age-based).

4. New tax on earnings in transition to retirement (TTR) income streams

From 1 July, earnings in TTR arrangements will be subject to a concessional rate of tax up to 15% – the same rate paid on earnings in your super accumulation account. This change will apply to both new and existing TTRs. Currently, earnings on super in TTRs are tax free – like earnings in full account-based pension accounts.

5. Improved access to concessional contributions

From 1 July 2017, the Government will allow all individuals under the age of 65, and those aged 65 to 74 who meet the work test, to claim a tax deduction for personal contributions to eligible superannuation funds up to the concessional contributions cap.

Currently, an income tax deduction for personal superannuation contributions is only available to people who earn less than 10% of their income from salary or wages. This limits the ability for people in certain work arrangements to benefit from concessional contributions to their superannuation. Under the new arrangements, more individuals will be able to make concessional personal contributions up to the annual cap.

This means that employees can now make tax deductible super contributions without needing to do this through a salary sacrifice. The reform will benefit individuals who are partially self–employed and partially wage and salary earners – such as self–employed contractors, individuals employed by small businesses or freelancers – as well as individuals whose employers do not offer salary sacrifice arrangements.

6. Greater access to the tax rebate on spouse contributions

From 1 July, 2017 you can apply to claim a rebate of up to $540 if you make super contributions for a spouse whose total earnings are less than $40,000. Currently the rebate is only claimable if your spouse’s earnings are less than $13,800.

7. Allowing catch up concessional contributions

From 1 July 2018, the Government will help people ‘catch up’ their superannuation contributions by allowing individuals with a total superannuation balance of less than $500,000 just before the beginning of a financial year to carry forward unused concessional cap space (for up to 5 years) to use if they have the capacity and choose to do so.

In 2019–20, this will help people who take time out of work, whose income varies considerably from one year to the next, or who find their circumstances have changed and are in a position to increase their contributions to superannuation.

Individuals aged 65 to 74 who meet the work test will be eligible to access these new arrangements.

Further help:

If you have concerns about how these superannuation reforms will effect your retirement or investment plans, Marsh & Partners SMSF advisors are able to help.

You can contact us on 07 3023 4800 or at mail@marshpartners.com.au

Share this article on LinkedIn:

Subscribe to our newsletter:

Get tax updates, business advice and seminar invitations delivered straight to your inbox.

GENERAL ADVICE WARNING: This information has been prepared without taking into account your objectives, financial situation or needs. Because of this, you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation or needs. We suggest you obtain specific financial advice from a licensed financial advisor.